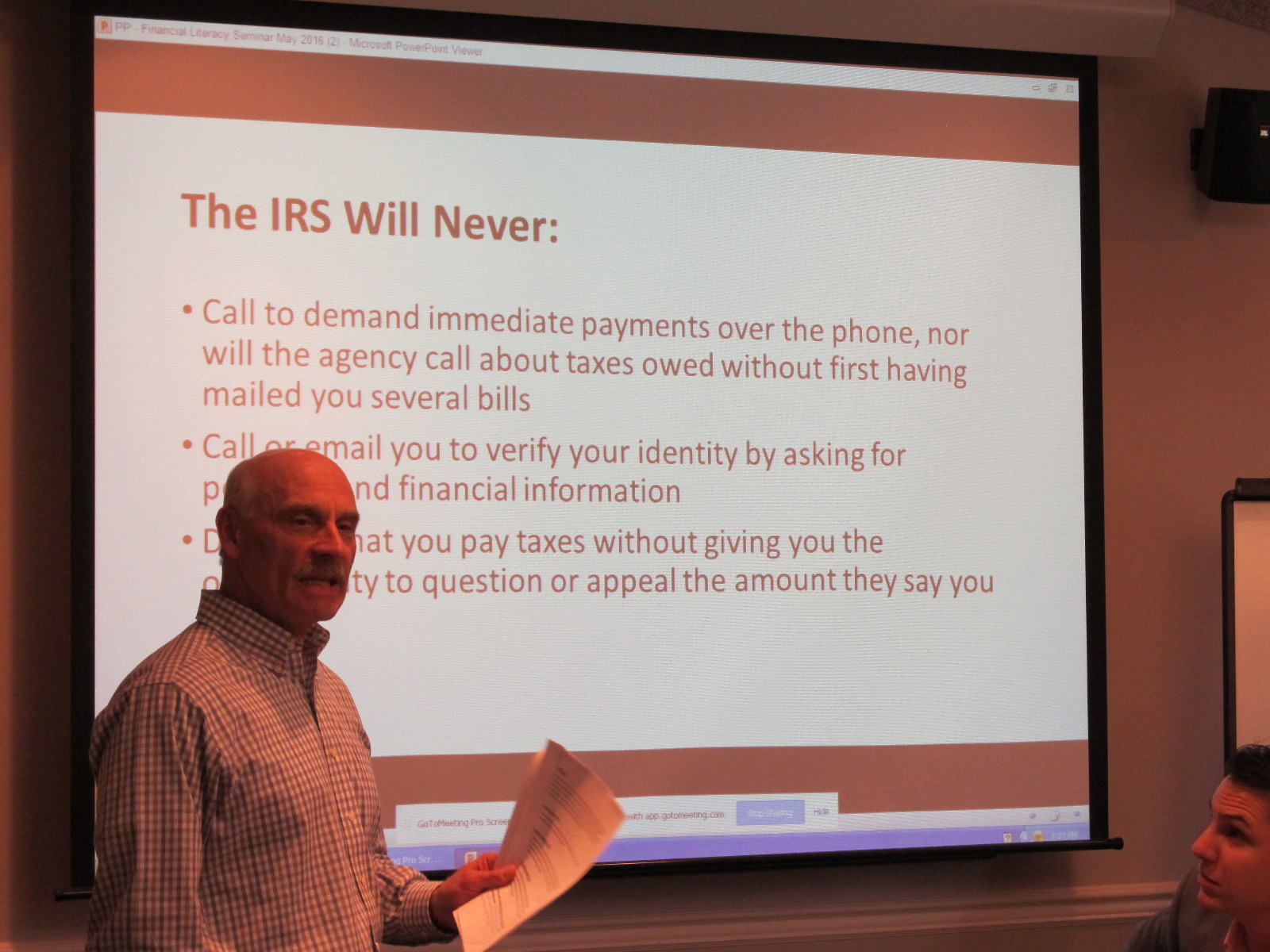

With incidents of financial fraud on the rise, the second session in our Wealth Management division’s Financial Literacy series focused on “Financial Self-Defense.” The hour-long seminar focused on three main areas of financial fraud: preying on senior citizens, tax-related fraud, and general financial fraud. Today’s recap covering red flags for senior citizens is the first in a series of blog posts recapping the seminar.

Top Ten Red Flags of Senior Citizen Financial Fraud

#1. “He said he was certified to help people like me.”

If the financial advisor is telling you it’s normal procedure also to be the custodian of your account, be aware that this is not a financial management best practice. Two different entities should serve these roles.

#2. “Don’t worry about the details; they’ll just confuse you.”

Wrong. You have the right to get a second opinion from a trusted professional. If you don’t understand what is being said, don’t buy it.

#3. “You’re Invited! Wine, Dine and Learn!”

You have probably been invited to at least one of these events. You’re promised a nice meal and a presentation of the advisor’s services. Be aware, this type of practitioner usually counts on high up-front commissions. Don’t feel obligated to please by making a decision you could regret later.

#4. “You don’t want what you leave to your family or charity to be eaten away by taxes or fees, do you?”

Don’t give in to this tactic, designed to pressure or scare you into making a decision that is not in your best interest. Just because a so-called expert recommends it doesn’t mean it’s right for you.

#5. “Do you need more income from safe fixed-income investments? We’ll show you how!”

Beware these promises of high returns on small investments. If it sounds too good to be true, it’s probably not legitimate or safe.

#6. “He’s one of us. I’m sure you can trust him.”

Always reserve the right to do your research. Even if an advisor is recommended from within your social circle, take the time to learn more, get a second opinion from an objective third party. Don’t confuse familiarity with trust.

#7. “I’ll take care of all the paperwork.”

Sounds perfect, right? Wrong. You want to see and understand all paperwork dealing with your money. The final sign-off should always be yours.

#8. “All of my clients in this fund are making a lot of money.”

Don’t feel pressure to follow the masses. In most cases, this tactic is designed to benefit the advisor more than you. Make sure the money others are making isn’t yours.

#9. “I’ve got a much better idea for your money.”

This perspective is a likely precursor to what’s known as “churning,” or excessively trading your account so the advisor receives more commission. Get as much information as possible about their proposal and get it checked.

#10. “Stop paying the bank for your house. Let the bank pay you!”

A reverse mortgage might sound like a great deal but be careful. Don’t sign over the deed to your property and know that you don’t have to take the payment in a lump sum. As a homeowner, you have rights. Make sure you know what they are before entering into this kind of agreement.

In any dealings with a financial advisor, there is no need for you to feel rushed or pressured into making a decision. Transparency and third party accountability are key. If you have questions, we would be happy to help. Learn more at www.canoncapital.com or call 215-723-4881.